Why 2026 Energy Management Mandates Shape C-Suite Priorities: An Operational Framework for Energy Management in EU Markets & an enterprise intelligence strategy for European operations balancing cost, compliance, and structural competitiveness.

KEY TAKEAWAYS

- EU energy pressures have moved from price-shock territory into permanent cost and competitiveness territory.

- CSRD, CBAM, and ETS2 are forcing operational change inside companies, not just reporting work.

- Disconnected workstreams create direct financial exposure under active 2026 CBAM certificate obligations and ESRS E1 reporting reviews.

- Modern energy management is no longer a procurement problem; it is an operational visibility and data discipline problem.

- The enterprises winning in energy management 2026 are those integrating cost, consumption, and carbon under one unified operational system.

A few years ago, I was listening to a keynote from the International Energy Agency’s Fatih Birol where he said IEA had started asking job candidates an interview question:

What three actions would you take if the Strait of Hormuz was closed?

Most candidates couldn’t fathom why the strait would ever close. But as we now know, by 2025, the question has become a real planning scenario.

I think about that anecdote often these days. It’s really telling of how the conversation around energy greatly shifted.

Three forces have been changing the game:

→ The explosive growth of demand for artificial intelligence and the data centers powering it have introduced electricity loads that supply is not growing fast enough to meet.

→ Supply-side constraint and the structural pivot away from fossil fuels has made “energy security” a term we now use in boardrooms.

→ Geopolitical instability has put a new question on every CFO’s desk: will we be able to source the energy we need in the years ahead?

Everyone’s attention has turned to renewables, and that direction is not reversing. But the renewable transition is itself an indicator of why this conversation is no longer optional.

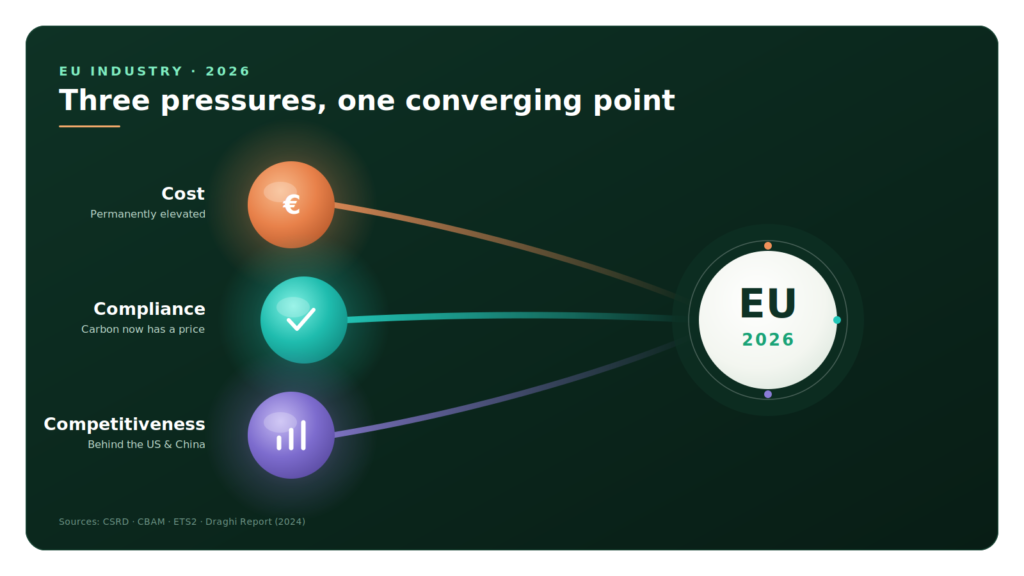

For companies executing energy management in EU territories, three structural pressures are converging at once:

- Cost: energy prices have eased from their 2022 peaks but settled into a permanently elevated band.

- Compliance: CSRD, SKDM, and ETS2 have moved beyond reporting exercises into operational mandates that put a price on carbon.

- Competitiveness: EU industrial energy costs continue to outpace those in the United States and China, creating a structural disadvantage that the Draghi Report (2024) flagged as one of Europe’s most pressing economic issues.

These three pressures rarely arrive separately. And we’ve been seeing that most companies feel them in combination.

Which Industrial Sectors Are Most Impacted by Energy Management in EU Frameworks?

The companies that feel the cost pressure most acutely are often the ones that cannot pass it on to customers. Producers of cement, ceramic, glass, textile, fertilizer, and similar globally-priced commodities cannot simply raise their selling price when energy gets more expensive.

The cost has to be absorbed elsewhere: through reduced margins, cut production, or postponed investment.

Across the EU, industrial gas demand remains well below pre-pandemic levels. That tells us the pressure is not just showing up in prices. It is showing up in demand destruction and competitiveness loss.

The sectors still feeling this most acutely:

| Affected Sector | Core 2026 Energy Pressure Point | Primary Cost Driver |

| Heavy Industry (Cement, Steel, Glass, Ceramics) | Inability to pass costs down global commodity supply chains. | Structural gas price floor & raw process heat demands. |

| Chemicals & Agri-Business (Fertilizer, Plastics) | Structural supply-side pivoting away from fossil feedstocks. | Permanently elevated baseline electricity bands. |

| Manufacturing & Cold Chain (Food Processing, Textiles) | High dependency on volatile peak-load pricing windows. | Sub-meter infrastructure deficits & thermal leaks. |

| Digital Infrastructure (Data Centers, AI Compute) | Exponentially scaling load requirements outstripping grid supply. | High baseline load matching requirements. |

What does this tell us? For energy-import-dependent economies, the problem is no longer the sudden price shock of 2022. It is the persistent cost pressure and competitive disadvantage that has settled in since.

How EmpCo and CSRD Transformed Energy Management 2026 Parameters

Among the CFOs and COOs I work with, the pressure from CSRD, CBAM, and ETS2 lands in the same place:

The market is now forcing companies to credibly decarbonize, with accountability, in ways that can be audited.

Compliance is no longer a matter of appearing decarbonized but actually applying real decarbonization practices.

Cosmetic policies and inflated sustainability ratings, the kind that have shielded slow movers for the past decade, are being closed off. The directives now define measurement and tracking methods clearly. Even environmental marketing claims are bound by tighter rules. Producing greenwashed “eco” products is becoming impossible.

“With the EU’s Empowering Consumers Directive (EmpCo – Directive EU 2024/825) becoming fully binding on September 27, 2026, cosmetic sustainability ratings and vague environmental claims carry active legal liabilities. Under EmpCo, product-level ‘climate-neutral’ or ‘CO2-compensated’ claims based on carbon offsetting outside the direct value chain are entirely prohibited. Furthermore, any forward-looking environmental commitments require an explicit implementation plan with measurable targets and mandatory independent third-party verification. In jurisdictions like Germany (via the updated UWG), non-compliance risks severe financial penalties of up to 4% of annual global turnover.”

Meaning we’ll likely be seeing less vaguely green products like this infamous Coca Cola ad.

With that in mind, the hardest part of CSRD compliance comes after the disclosure: building the operational discipline the disclosure assumes.

What operations must recognize is that sustainable energy management expectations in 2026 require real, granular measurement systems behind them, which is hard to establish when most sustainability departments have been the orphan child of the company for years, kept around for marketing reasons but rarely integrated into operational decision-making.

In 2026, that position has become hard to justify. Sustainability is now a C-suite responsibility because the regulation has made it one.

SKDM and ETS2 sharpen this in a different way.

By putting a direct price on carbon, they make decarbonization a financial conversation. Heavy industry running legacy production methods has to absorb a new cost line or rebuild its product portfolio. Rebuilding means new production principles, new R&D, new pricing, new customers, and new internal expertise.

The breaking point is, none of that is comfortable, none of it is fast, and none of it is optional.

Why Fragmented Energy and Carbon Data Streams Create Audit Risks Under ESRS E1

Most companies still treat energy management, fuel management, and supply chain emissions as three separate disciplines under three different teams. They look like separate problems.

They are not.

They are three legs of the same operational stool, all outputs of the same activities the company performs every day.

When energy, fuel, and supply chain are managed separately, the numerical results may look complete on paper, but they cannot be evaluated against any meaningful decarbonization picture. You end up with disclosures, not strategy.

For exporters subject to CBAM, this gap becomes a financial liability.

The transitional reporting phase for the Carbon Border Adjustment Mechanism (CBAM) is officially over. As of January 1, 2026, the definitive financial phase is live, requiring importers to purchase physical CBAM certificates tied directly to fluctuating EU ETS carbon prices (~€80–90/ton). Because default emission values now incur heavy financial penalties, primary, auditable utility and production data have shifted from a disclosure preference to a direct margin-protection requirement.

Common sources of bad data show up everywhere:

- production lines on shared meters,

- generators backing up shared common areas,

- market-based reporting with weak certificate backing,

- monthly consumption reports that don’t reconcile to invoices

Each of these is a path from sloppy energy measurement to disclosable carbon numbers that won’t withstand scrutiny.

The thing is, bad energy data producing problematic carbon reports is a foundational reality. It is also a fixable one, but only when the energy and carbon workstreams stop being treated as separate budgets, separate teams, and separate technology stacks.

The cost mistake that repeats across every sector

If you asked me the most consistent mistake I see across EU companies, my answer without hesitation would be: they still treat energy management as a purchasing cost, not as an operationally manageable variable.

The boardroom conversation is usually: “can we get a better electricity or gas tariff?”

The conversation that would actually change the bill is: “why are we using this much energy, in which processes, at which hours, and is it necessary?”

The pattern repeats regardless of sector:

- A factory negotiates a better supply contract but cannot identify which line creates peak load.

- A retail chain monitors store-level bills but cannot separate HVAC, lighting, and refrigeration.

- A food producer complains about gas costs but does not measure boiler efficiency, steam losses, or waste heat potential.

- An office portfolio buys renewable electricity certificates but cannot explain why per-square-meter consumption keeps rising.

→ The company believes it has an energy price problem.

→ The actual problem, in most cases, is an energy visibility problem.

Tariff matters, of course. But the companies that adapted most successfully after 2022 did not stop at renegotiating supply contracts. They built control over the details that actually make the difference:

Consumption profiles, load shapes, sub-meter infrastructure, baselines, facility-level accountability, investment prioritization, and other sector-specific variables.

Let’s talk more about that:

What companies that have figured this out actually do

When I walk into a company doing this well, the difference is rarely in the technology. It is in the management discipline that came before the technology.

Once you recognize certain facts of the current energy market and how it should reflect to your processes, energy management becomes easier.

5 concepts that really drive efficiency when you recognize them are:

1. Energy data is not anyone’s side job.

Consumption is tracked at facility, line, process, equipment, and product level, not just from invoices. Finance, operations, procurement, and sustainability are all looking at the same data.

No one is keeping a separate Excel.

2. Consumption is tied to production.

Mature operators do not ask “how many kWh this month?”

They ask “what did we consume per ton, per product group, per square meter, per shift, per cooled volume?”

This is how they separate production-driven consumption growth from inefficiency-driven consumption growth.

3. Baseload and peak load are managed deliberately.

They identify the systems still drawing energy at night, on weekends, and during non-production hours. They know which equipment, which shift, and which process drives peak demand.

The most important thing to understand here is that these companies don’t necessarily aim for reducing total consumption but rather reshaping the structure of energy cost for maximum efficiency.

4. Energy projects are managed like an investment portfolio.

To emphasize how much a big picture POV matters:

Waste heat recovery, compressed air leak reduction, boiler efficiency, chiller optimization, motor upgrades, rooftop solar, PPAs, batteries, electrification: all evaluated through the same lens.

Investment amount, payback period, emission reduction, operational risk, and reporting impact, side by side.

5. Energy data is not separated from carbon data.

Credible CBAM exposure calculation, defensible CSRD numbers, Scope 1 and 2 reporting, product carbon footprints, and lifecycle assessments all rest on the same underlying energy data.

Mature operators run their meter infrastructure, data ownership, invoice reconciliation, emission factor selection, production allocation, and data quality controls as a single system.

In companies still figuring this out, the picture is inverted:

Energy sits with procurement as a tariff problem.

Operations tracks consumption in its own silo. Sustainability requests data when the report is due. Finance pays the invoice. No one owns the full picture. The company knows exactly what it pays, but it has no idea what it should be consuming.

What energy management software should actually do: criteria for selecting modern energy management software

If a CFO asked me to describe in one sentence what energy management software should do for them, my answer would be this:

Identify the inefficient points in our operations and reduce our energy costs.

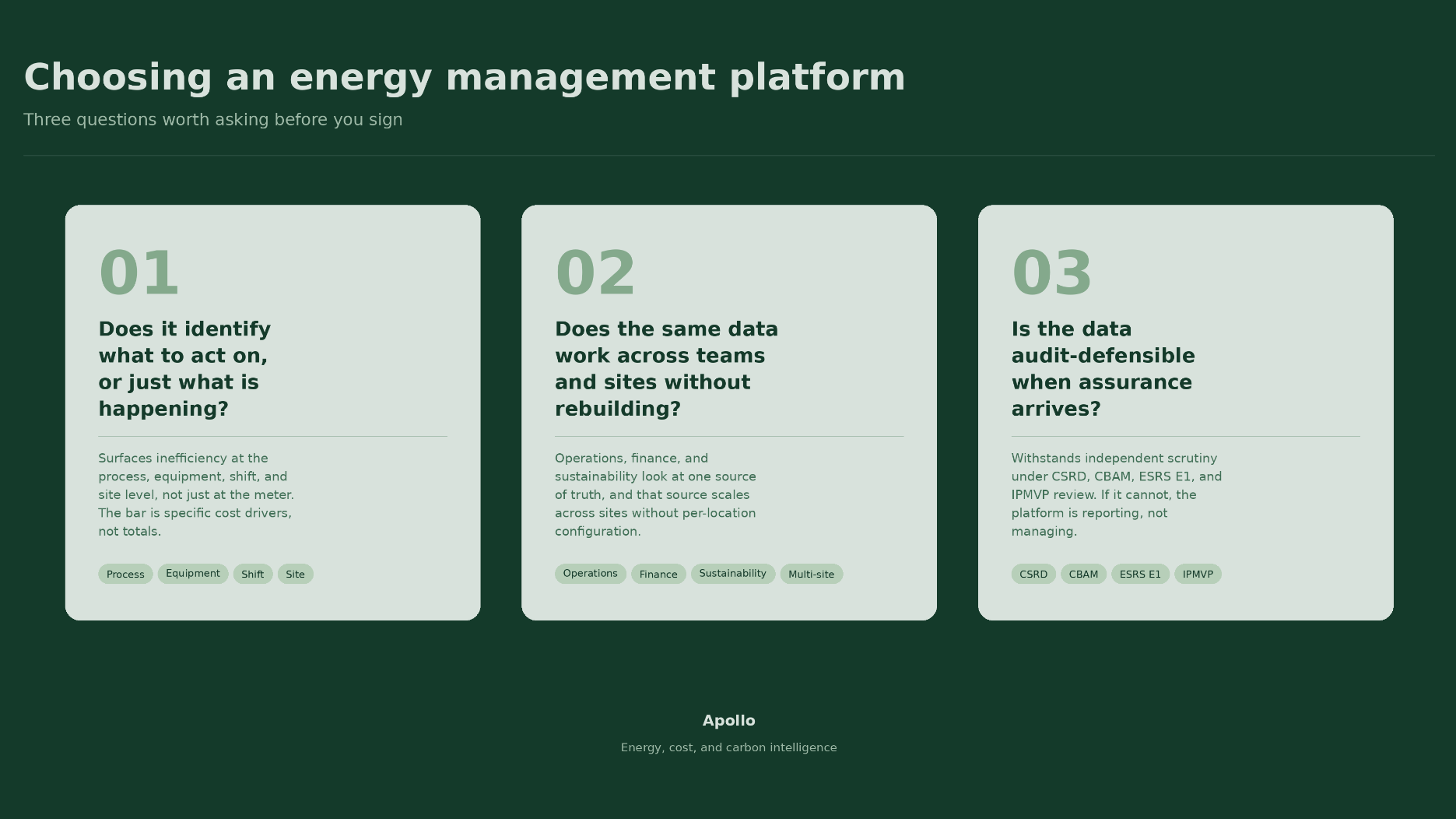

That single criterion underpins how to evaluate a platform. Three questions are worth asking:

- Does it identify what to act on, or just what is happening? The platform should surface inefficiency at process, equipment, shift, and site level, not just at the meter. The bar is whether it tells you which specific cost drivers to address, not just what your total consumption looks like.

- Does the same data work across teams and sites without rebuilding? Operations, finance, and sustainability should be looking at one source of truth, and that source should scale across sites without bespoke configuration per location.

- Is the data audit-defensible when assurance arrives? Whether the reviewer is checking CSRD, CBAM, ESRS E1 disclosures, or IPMVP measurement and verification documentation, the platform’s data should withstand independent scrutiny. If it cannot, the platform is reporting, not managing.

Platforms built around these criteria, Apollo among them, focus on the integrated energy-cost-carbon discipline rather than on any one of the three in isolation. That focus is what matches the operational reality CFOs and COOs are now navigating.

The forward view

2026 is not the year to delay.

The cost pressure, the regulatory pressure, and the competitiveness pressure are converging at the same time, and they are doing so in a way that compounds. Each year a company defers building real energy management discipline, the gap between it and its better-prepared competitors widens.

Energy has become the operational discipline that determines whether a company stays competitive in the EU after 2026.

The companies that recognize this and act on it now are buying themselves multi-year structural advantage.

Energy Management 2026 Action Plan: Critical Priorities for Energy Management in EU Markets

Before shifting market dynamics and tightening regulatory parameters compound this quarter, enterprise decision-makers must optimize their internal energy management frameworks against five immediate updates:

Utility billing errors and peak anomalies are inflating operational costs

Deadline: Immediate

Action: Automate invoice validation to eliminate contract mismatches and reactive power penalties.

Hidden baseload leaks and process inefficiencies escape primary meters.

Deadline: Sürekli

Action: Deploy sub-metering and shift analysis to isolate asset-level waste.

Retrospective spreadsheet estimates will fail upcoming corporate transparency audits.

Deadline: 2026 Fiscal Cycle

Action: Secure granular data lineage to clear strict ESRS E1 limited assurance reviews.

The financial CBAM phase is live, taxing embedded imports at an official €75.36/tCO₂.

Deadline: Active Now

Action: Use primary production-line data instead of heavily penalized default values to protect margins.

Vague environmental branding triggers catastrophic greenwashing liabilities.

Deadline: September 27, 2026

Action: Eliminate unverified “green” labels to avoid EmpCo directive fines of up to 4% global turnover.

Don’t know where to start? Let’s talk.

Book a demo today!

Frequently Asked Questions

How does CSRD impact enterprise energy data requirements in 2026?

Under the Corporate Sustainability Reporting Directive, compliance reviews heavily scrutinize the data lineage behind ESRS E1 disclosures. Companies must transition away from estimates. Achieving limited assurance requires granular, auditable primary data linking facility-level energy consumption directly to Scope 1, 2, and 3 emissions tracking, rendering disconnected spreadsheets an active compliance risk.

What are the financial implications of the active CBAM phase in 2026?

The transitional phase is over, meaning EU importers now face active financial obligations to purchase CBAM certificates tied directly to EU ETS carbon prices. Because relying on default emission values incurs punitive financial markups, verifying embedded production-line emissions with primary, auditable energy data is now a critical prerequisite to safeguard corporate profit margins.

What is the enforcement deadline and penalty for the EU EmpCo directive?

The Empowering Consumers Directive becomes fully enforceable across all EU member states on September 27, 2026. After this deadline, general environmental claims are illegal unless supported by verified environmental performance profiles. Non-compliance carries severe legal exposure, including active financial penalties reaching up to 4% of an enterprise’s annual global turnover.

How do energy management and energy procurement differ structurally?

Energy procurement focuses on the commercial transaction, securing the best per-unit commodity tariffs under favorable contract terms. Conversely, energy management is an operational intelligence discipline centered on understanding why, where, and when energy is consumed. While procurement reduces the price per unit, active management permanently lowers the actual volume of units required.

What technical criteria should an enterprise look for in an energy platform?

In 2026, platforms must seamlessly integrate energy, cost, and carbon tracking. Ensure the software offers automated invoice validation to prevent reactive capacity penalties, provides granular anomaly detection at the asset level rather than just the primary meter, and delivers audit-defensible carbon data compliant with ESRS E1 limited assurance and IPMVP validation protocols.